Introduction: The Shifting Sands of GST Compliance

The Indian Goods and Services Tax (GST) landscape is undergoing an automated structural evolution, transitioning rapidly from aggregate self-reporting to transactional, real-time matching. Historically, the administration of interest under Section 50 of the Central Goods and Services Tax (CGST) Act, 2017, was plagued by bitter disputes regarding whether interest should be levied on the gross liability or strictly on the net cash portion, and how early deposits in the Electronic Cash Ledger (ECL) should be treated. Delayed invoice reporting under GST is increasingly becoming a major litigation issue across multiple states.

While the retrospective insertion of the proviso to Section 50(1) (effective from July 1, 2017) clarified that interest applies only to the net cash portion paid via the ECL, the actual procedural mechanics long remained highly manual and prone to administrative inconsistency. This issue of delayed invoice reporting under GST has gained significant attention after the 2026 GST portal updates introduced automated invoice-period matching and retrospective scrutiny mechanisms.

However, this enforcement landscape shifted dramatically with the implementation of the January 2026 GST portal updates. The Goods and Services Tax Network (GSTN) integrated automated interest calculation engines and structured tracing tools directly into Form GSTR-3B. While these features were engineered to streamline current compliance, they have triggered a severe and unintended side effect: a nationwide wave of retrospective interest notices under Section 50(1). This issue is distinct from mere late filing of Form GSTR-1 and primarily concerns invoices pertaining to one tax period being reported in a subsequent month.

Quick Summary

- GST departments are issuing retrospective interest notices for invoices uploaded in subsequent GSTR-1 periods.

- The notices rely on automated invoice-period matching introduced after GST portal updates in 2026. Several High Courts have held that delayed invoice reporting alone does not automatically justify interest.

- Taxpayers can defend themselves using ITC availability, ECL deposit timelines, and procedural violations.

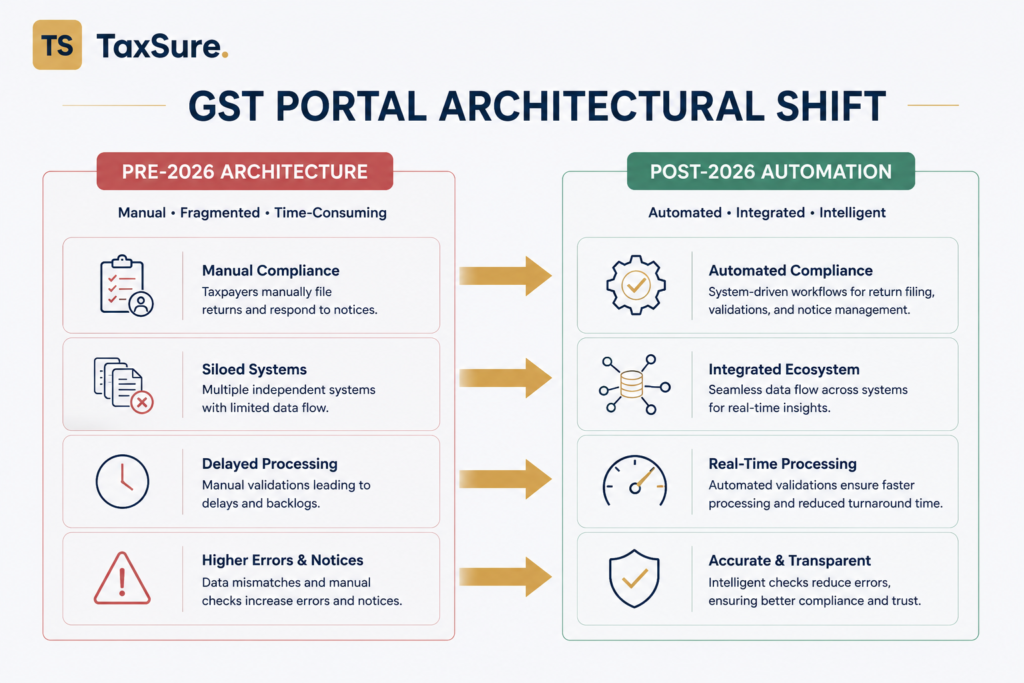

The 2026 Portal Enhancements: From Compliance Tool to Retroactive Audit Weapon

The January 2026 portal updates introduced two powerful advanced tracking mechanisms that completely revolutionized compliance enforcement across all states:

- Automated Interest Calculation Engine: The portal now tracks the “minimum cash balance” in the taxpayer’s ECL from the statutory due date of the return until the actual offset date, automatically granting a deduction for early deposits in line with the proviso to Rule 88B(1) of the CGST Rules, 2017. However, this automated system calculation in Table 5.1 of GSTR-3B is non-editable downward, blocking taxpayers from manually reducing the computed interest value.

- Mandatory “Tax Liability Breakup” Framework: From the January 2026 return filing cycle onwards, the portal matches document-level dates reported in Form GSTR-1, GSTR-1A, or the Invoice Furnishing Facility (IFF) against the tax period of the current GSTR-3B. If an invoice with a previous period’s date is uploaded in the current month’s GSTR-1, the system automatically flags this as a prior-period supply, segregates the liability, and auto-populates the “Tax Liability Breakup” table in GSTR-3B. Under this revised sequence, filing is blocked until the taxpayer confirms, saves, and offsets these segregated values.

How Delayed Invoice Reporting Is Triggering GST Interest Notices

The advanced transactional tracing and data-segregation backend engines developed for these 2026 updates are now being applied retrospectively by state tax administrations. By executing database queries on historical GSTR-1 and GSTR-3B records for prior financial years, tax departments can instantly identify timing differences where invoice dates in Form GSTR-1 precede the return period of the Form GSTR-3B in which the corresponding tax liability was discharged.

Businesses must understand the legal implications of delayed invoice reporting under GST before responding to automated notices.

In short, technical features built for real-time tracking have been repurposed as retroactive database auditing tools to mine historical records and generate bulk, automated interest demands.

GST Portal Architectural Shift (Pre vs. Post 2026)

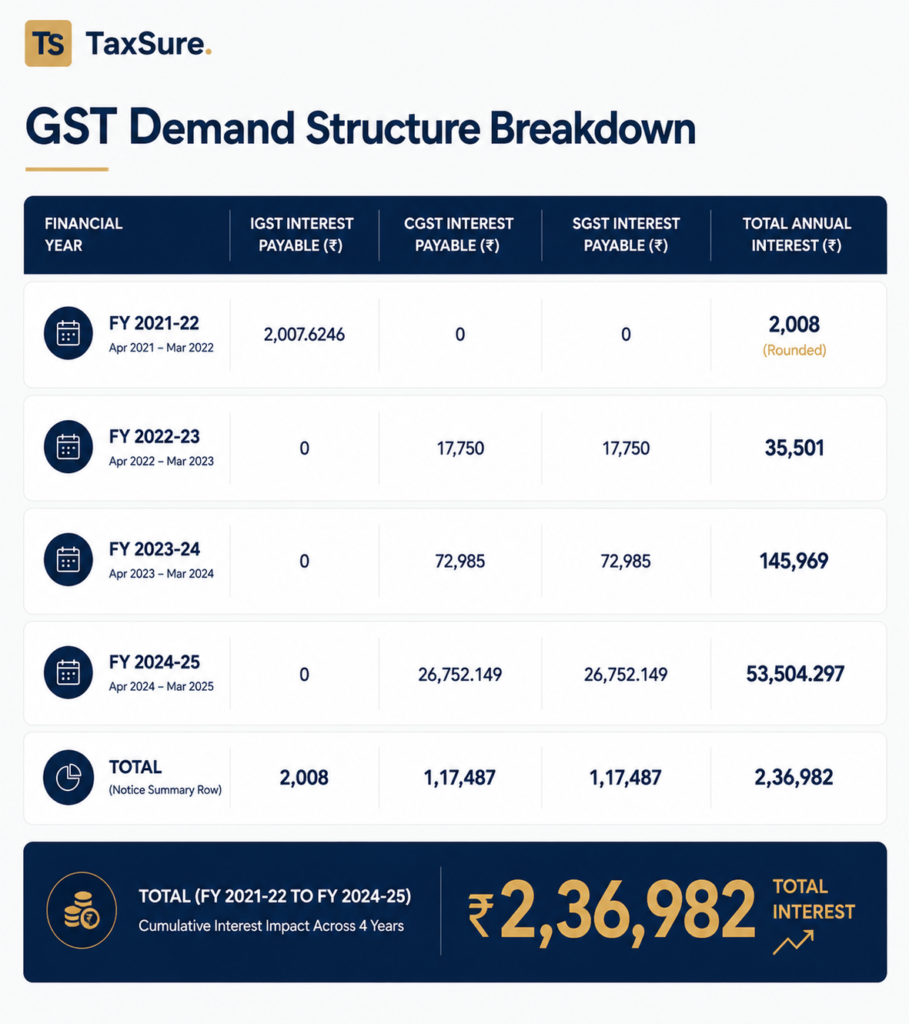

Empirical Analysis: The Assam State Tax Department’s Notice Structure

An examination of recent sample notices issued by the State Tax Department of Assam reveals the systematic application of this automated data mining to historical filings. The notices typically target four distinct financial years—from FY 2021-22 to FY 2024-25—asserting that a delay in uploading invoices in Form GSTR-1 resulted in a delayed payment of tax, thereby attracting interest at 18% per annum under Section 50(1).

Quantification of the Demand

Consider the following consolidated interest demand pattern split across multiple tax heads and financial periods:

Critical System Vulnerabilities & Formatting Anomalies

Taxpayers must watch out for a highly specific formatting anomaly frequently visible in the summary rows of these automated departmental notices. As shown in the empirical data above, figures are sometimes represented with the period (.) used interchangeably with the comma as a digit group separator to denote thousands and lakhs (e.g., 1.17.487 and 2.36.982), while simultaneously using standard decimals within the exact same table body.

This formatting inconsistency poses a high risk of parsing errors if processed by automated corporate tax reconciliation software, potentially misinterpreting an integer value of ₹1,17,487 as a decimal ₹1.17.

Furthermore, these automated portal calculations are far from infallible. During the March 2026 return filing cycle, a major technical glitch occurred where the interest for the February 2026 tax period was auto-populated without applying the mandatory “minimum cash balance” deduction. In response, the GSTN had to hastily introduce a “RE-COMPUTE INTEREST” button within Table 5.1 to trigger a recalculation based on actual daily ledger data. This glitch provides vital evidence for taxpayers: it demonstrates that system-generated portal calculations cannot be defended blindly by the department as inherently correct or legally final.

Deconstructing the Department’s Legal Fallacies

The department’s notices typically cite Section 37(1) of the CGST and respective State GST Acts (mandating timely filing of outward supplies in GSTR-1) along with Section 39(1) (obligating taxpayers to declare tax liability and discharge it through GSTR-3B).

The core departmental allegation states that “certain invoices were reported with delay, resulting in deferment in payment of applicable tax. Accordingly, interest is leviable for the period of such delay.” To support this, the authorities rely on a fundamental conceptual leap: “the liability to pay tax arises at the time of supply in accordance with the provisions of the Act.”

This represents a severe misapplication of the “Time of Supply” rules (Sections 12 and 13). The department is attempting to use the time of supply to override the specific “period prescribed” for payment under Section 50(1).

Under the statutory scheme of GST:

- Tax is declared and paid through Form GSTR-3B under Section 39, which operates on its own explicitly prescribed statutory due dates.

- As long as the tax is paid via GSTR-3B on time, a reporting delay in GSTR-1 does not constitute a payment delay.

By arguing that a delay in GSTR-1 filing automatically postpones the payment of tax, authorities unlawfully conflate a reporting delay under Section 37 with a payment delay under Section 50(1).

Legal Defenses Against Delayed Invoice Reporting Notices

To successfully dispute these automated interest demands, taxpayers across all jurisdictions can build a robust case around several well-established judicial doctrines:

1. The Compensatory Principle and Continuous ITC Availability

Interest under Section 50 is strictly compensatory in nature, designed to compensate the exchequer for an actual loss of revenue; it is not a penalty. Consequently, if a taxpayer maintains a continuous, sufficient balance in their Electronic Credit Ledger (ECRL / Input Tax Credit) that exceeds the tax liability of the delayed invoice from the original due date until the invoice is reported, the exchequer suffers no loss of revenue.

- Landmark Precedents: The Delhi High Court in M/s. Surya Roshni Ltd. v. Commissioner of CGST, Delhi (2021) and the Gujarat High Court in M/s. Bajaj Electricals Ltd. v. Union of India (2022) ruled that delayed reporting of an invoice does not attract interest if the output tax liability was fully covered by available ITC.

- Board Clarifications: This position is strongly reinforced by CBIC Circular No. 125/44/2019-GST and Circular No. 238/32/2024-GST, which clarify that interest does not apply to transactions settled through available ITC.

2. ECL Deposits Constitute Immediate Payment to the Government

When a taxpayer deposits cash into the ECL under Section 49(1), the funds are transferred directly from the taxpayer’s bank account to the government’s account. Once deposited, the taxpayer cannot withdraw or use these funds for non-GST purposes, meaning they are legally committed to the exchequer.

- Landmark Precedents: In Arya Cotton Industries v. Union of India (Gujarat High Court, June 14, 2024), the court ruled that once cash is deposited into the ECL, the taxpayer’s liability stands discharged on that date. The subsequent debit to the ECL during GSTR-3B filing is merely an accounting adjustment. Charging interest on funds already residing in the government’s account turns a compensatory levy into an unauthorized penalty. This stance was further solidified by Symphony Limited & Anr. v. Union of India (Gujarat High Court, 2025) and Eicher Motors Limited v. Union of India (Madras High Court, 2024).

3. Inapplicability of Direct Recovery under Section 75(12)

The department frequently attempts to bypass standard notice and hearing requirements of Section 73 by classifying GSTR-1/GSTR-3B mismatches as “unpaid self-assessed tax” under Section 75(12), permitting direct recovery under Section 79.

- Landmark Precedent: In Kuddus Ali v. Assistant Commissioner of Central Tax (Calcutta High Court, 2025), the court ruled that Section 75(12) applies only when the self-assessed tax declared in GSTR-1 is completely omitted from GSTR-3B. If the liability was eventually declared and paid in GSTR-3B (even with timing differences), the direct recovery provisions cannot be used. Bypassing the formal Show Cause Notice (SCN) and personal hearing requirements violates the principles of natural justice.

4. Absolute Exclusion from the Section 128A Amnesty Scheme

Taxpayers must note that they cannot resolve disputes over delayed GSTR-1 uploading through the Section 128A Amnesty Scheme (Finance Act, 2024). CBIC Circular No. 238/32/2024-GST (clarified in Circular No. 248/05/2025-GST) explicitly states that this amnesty waiver does not apply to interest demanded on account of delayed return filing or delayed reporting of supplies. The Board treats such interest as a liability on self-assessed returns under Section 75(12) rather than a tax demand under Section 73. Taxpayers must challenge these demands purely on their legal merits, using the Arya Cotton and Surya Roshni doctrines.

Strategic Judicial Blueprints: Key High Court Precedents

While these defense pillars stand strong across India, specific rulings from regional benches—such as the Gauhati High Court—provide exceptionally rigorous and thorough blueprints for countering automated interest notices. These judgments serve as powerful persuasive authorities for businesses nationwide.

M/s ITI Ltd. vs Union of India & Ors. (The GSTR-1 Status Rule)

Addressing GSTR-1 and GSTR-3B mismatches and the use of Section 75(12), the High Court quashed automated demands and established baseline procedural safeguards:

- GSTR-1 is Not a Conclusive Self-Assessment: Form GSTR-1 is merely a statement of outward supplies and cannot be treated as a final, binding self-assessment of tax liability.

- Rule 88C is a Jurisdictional Prerequisite: In cases of GSTR-1/GSTR-3B discrepancies, the proper officer cannot bypass the mandatory intimation procedure under Rule 88C. Issuing Form GST DRC-01B to give the taxpayer an opportunity to explain the discrepancy is a jurisdictional prerequisite before any recovery action under Section 79 can be initiated.

MD Shoriful Islam vs. The State of Assam (Mandatory Detailed SCN)

The Court ruled that a GST demand cannot be based solely on a brief summary of an SCN in Form GST DRC-01. It held that the department must issue a proper, detailed text SCN under Section 73, and a personal hearing is strictly mandatory before any adverse order can be passed.

Santosh Kumar Harlalka vs State of Assam & Ors. (Lack of Machinery Provisions)

Applying the celebrated Supreme Court doctrine from India Carbon Ltd. v. State of Assam, the Court established that interest can only be levied and collected if the statute contains explicit and complete machinery provisions. Because Section 50(1) relies on a “prescribed period” which was not fully defined under the rules during earlier tax periods, demanding interest retrospectively for those periods is legally unsustainable.

Pepsico India Holdings vs. State of Assam (Scrutiny as a Mandatory Prerequisite)

The Court evaluated the mandatory workflow of assessment, ruling that scrutiny of returns under Section 61 and the issuance of an intimation in Form GST ASMT-10 are mandatory jurisdictional prerequisites before issuing a show-cause notice under Section 73(1). Any notice or interest demand issued without first following the ASMT-10 procedure is procedurally flawed and void for lack of jurisdiction.

How to Respond to a GST Interest Notice

If your business receives a retrospective interest notice for historical GSTR-1 reporting delays, follow this structured response protocol:

Step-by-Step Response Protocol:

- Step 1: Reconstruct Transactional Ledgers: Map every single invoice flagged in the notice to its actual date, value, and the GSTR-1 period in which it was declared. Identify the exact GSTR-3B return period and date when the tax liability was offset, reconstructing the daily balances of both the ECRL and ECL.

- Step 2: Document “No Revenue Loss” & ECL Timelines: Calculate whether the continuous balance in the ECRL was sufficient to cover the tax liability of the delayed invoices from their original due dates to their actual offset dates. If cash was used, identify the exact date the funds were deposited into the ECL to establish the payment date under the Arya Cotton doctrine.

- Step 3: Identify Procedural Flaws: Check if the notice was issued as a brief summary in Form GST DRC-01/DRC-01A without a proper, detailed text SCN , or if the department failed to issue Form GST ASMT-10 or follow the Rule 88C intimation procedure.

- Step 4: Draft and Submit a Structured Written Reply: Submit a detailed, point-by-point response on the GST portal.

Recommended Structure for Formal Replies:

- Preliminary Objections: Assert procedural violations such as the omission of Form GST ASMT-10 under Section 61 , notice vagueness violating natural justice , or the illegal bypass of Rule 88C intimation routes.

- Substantive Arguments on Merits: Present your certified ledger statements proving continuous ITC availability to showcase no revenue loss (Surya Roshni) or timely ECL cash deposits (Arya Cotton). Cite M/s ITI Ltd. to establish that Form GSTR-1 reporting delays cannot be treated as tax payment delays.

- Formal Prayers: Formally request that interest proceedings be dropped , demand a detailed invoice-wise calculation sheet , and request a mandatory personal hearing under Section 75(4).

Summary Defense Matrix for Tax Managers

| Notice Scenario | Department’s Claim | Taxpayer’s Core Legal Defense | Landmark High Court Precedent | Actionable Protocol |

| Invoices uploaded late in GSTR-1, but sufficient ITC was available on the original due date. | Interest is payable on the gross liability under Section 50(1) because the invoice was reported late. | Interest is compensatory. If available ITC exceeded the tax liability, the exchequer suffered no revenue loss. Under Surya Roshni, delayed reporting does not attract interest. | M/s ITI Ltd. v. Union of India (GSTR-1 is not a final self-assessment; errors do not alter actual liability). | Submit a certified ECRL ledger statement showing a continuous balance exceeding the flagged tax liability. |

| GSTR-3B filed late, but cash was deposited in the ECL on or before the statutory due date. | Interest is due from the statutory due date until the return filing date under Section 50(1). | Once cash is deposited into the ECL, it is legally committed to the government. Under Arya Cotton, the deposit date constitutes the payment date. | Pepsico India Holdings v. State of Assam (Authorities must act strictly within the statutory framework). | Prepare an ECL cash-flow statement showing that a sufficient balance was maintained in the ledger prior to the due date. |

| The department initiates direct bank recovery for GSTR-1/GSTR-3B mismatches without an SCN. | Direct recovery is authorized under Section 75(12) read with Section 79, as GSTR-1 discrepancies represent self-assessed tax. | Section 75(12) cannot be used once the GSTR-1 liabilities are declared and paid in GSTR-3B. Bypassing the SCN and Rule 88C violates natural justice. | M/s ITI Ltd. v. Union of India (Rule 88C is a mandatory jurisdictional prerequisite before recovery under Section 79). | File a formal objection citing ITI Ltd. If the department proceeds, file a Writ Petition before the High Court to stay recovery. |

| Standard interest notice received as a brief summary in Form Form GST DRC-01/DRC-01A. | Interest is a consequential, automatic levy under Section 50 and does not require detailed adjudication. | Even automatic levies require proper notice and calculation details. Vague and non-specific notices omit critical parameters and violate natural justice. | MD Shoriful Islam v. State of Assam (GST demands cannot be based solely on a DRC-01 summary; proper SCN is mandatory). | File a reply objecting to the vagueness of the notice. Demand a detailed, invoice-wise calculation sheet and a personal hearing. |

Disclaimer: This article is intended for informational and educational purposes for tax professionals, compliance managers, and corporate legal counsels. For specific tax disputes, please consult a registered indirect tax professional or a qualified GST litigation counsel.

Leave a Reply

We value your thoughts and would love to hear your perspective.