Executive Summary

As businesses adapt to shifting financial landscapes, optimizing corporate capital structures has become a critical priority for sustainable growth in 2026, the global corporate finance landscape continues to evolve, driven by a complex interplay of post-pandemic regulatory adjustments, volatile interest rate cycles, and the rapid digitization of capital markets. For Chief Financial Officers (CFOs), Treasurers, and Corporate Counsel, optimizing the capital stack is no longer merely an exercise in liquidity management; it is a critical differentiator for long-term solvency and shareholder value creation.

This white paper, presented by the Taxsure Corporate Advisory Group, provides a forensic analysis of the two pillars of non-equity capital—Debentures and Preference Shares. We examine their distinct characteristics, legal frameworks, taxation implications, and their specific application within the 2026 market environment, offering data-driven insights to guide your next capitalization event.

I. Introduction: The 2026 Capital Dilemma

The primary challenge facing corporate boards in 2026 is balancing flexibility, cost, and control. Traditional vanilla instruments are often insufficient for the nuanced risk-reward profiles demanded by modern institutional investors. CFOs must balance the need for non-dilutive, tax-deductible funding (Debt) against the requirement for permanent, equity-like, or rating-agency-friendly capital (Preference Equity).

The 2026 market is defined by a flatter yield curve compared to 2024, yet base rates remain structurally higher than the preceding decade. Furthermore, global tax harmonization efforts (such as Pillar Two) have added complexity to cross-border interest deductibility.

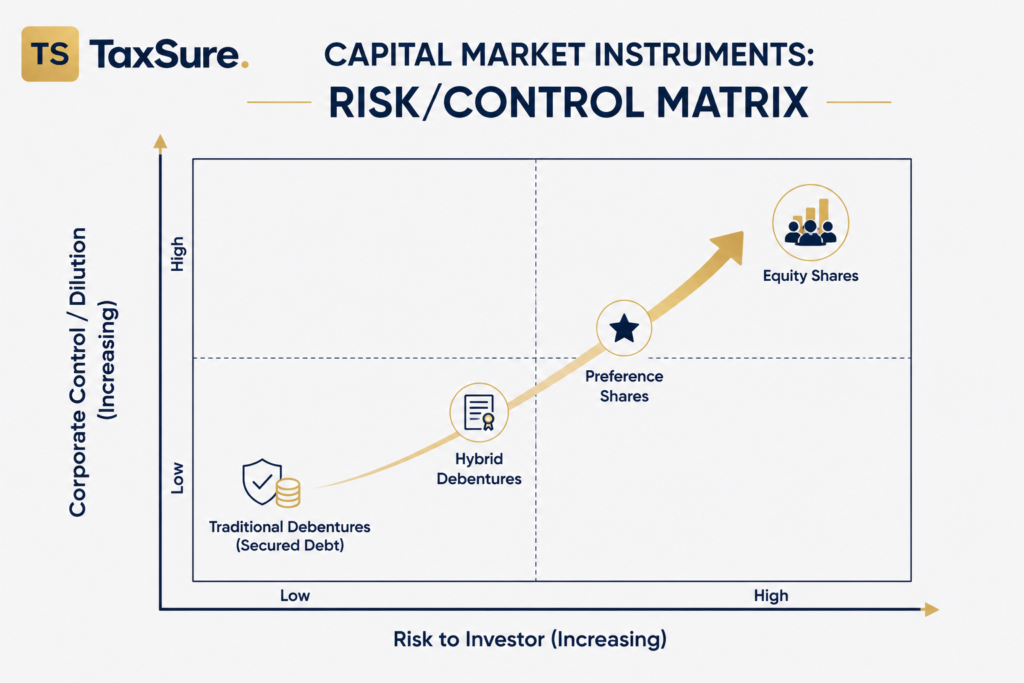

Before choosing an instrument, it is imperative to visualize the fundamental divergence in their nature. The core decision matrix—Risk vs. Control—remains the baseline for all subsequent analysis.

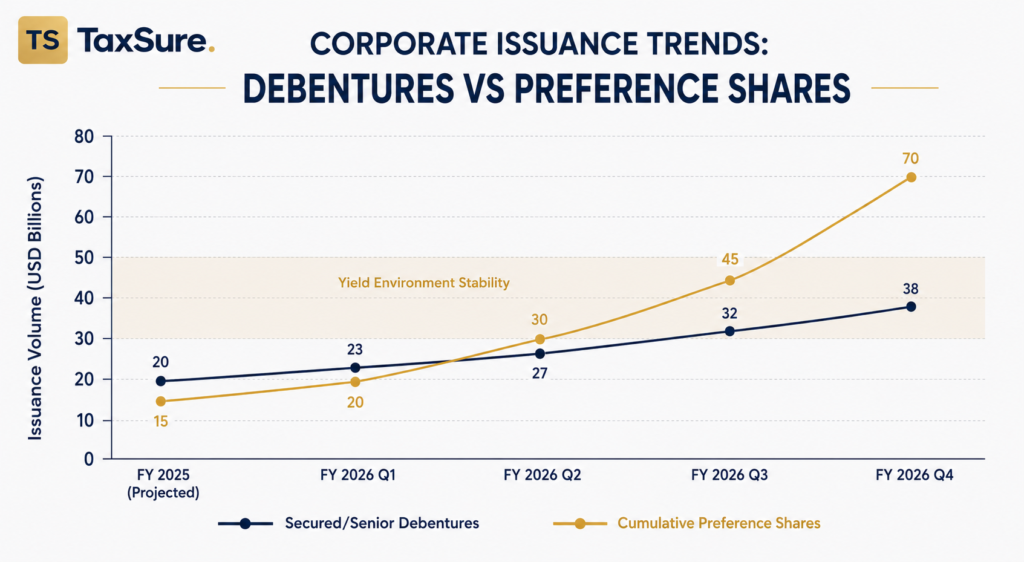

II. Anatomy of the 2026 Debenture Market

A debenture is a debt instrument, usually unsecured (though ‘secured debenture’ is sometimes used, typically in jurisdictions where this implies a floating charge), backed only by the general creditworthiness and reputation of the issuer. In 2026, the key defining characteristic remains the strict, contractually legally binding obligation to pay interest and repay principal.

Key Characteristics and 2026 Nuances:

- Status: Creditor. The holder is a creditor, not an owner. They have no voting rights under normal circumstances.

- Security: Most modern corporate debentures are unsecured, unsubordinated obligations, ranking pari passu with other senior unsecured debt. In asset-heavy industries (like Infrastructure/Real Estate), Secured Debentures (backed by a specific charge) are making a strong comeback in 2026, driven by lender demands for safety in uncertain sectors.

- Servicing (The Coupon): Interest payments are mandatory. Failure to pay constitutes a Default Event, which can trigger cross-default clauses in all other company debt and lead to insolvency proceedings. In 2026, floating-rate debentures indexed to robust risk-free rates (SOFR, SONIA) are dominant, but fixed-rate issuance is rising as issuers attempt to lock in perceived peaks.

- Tenor and Redemption: Debentures have a defined maturity date (e.g., 5, 10, or 30 years). Amortizing structures are increasingly favored in 2026 for mid-market issuers, reducing refinancing risk.

- Convertibility: A major 2026 trend is the revival of the Convertible Debenture. This hybrid offers the security of debt with an option to convert to equity, allowing issuers to lower their immediate coupon payment.

III. Preference Shares: The Resilient 2026 Equity Hybrid

Preference shares represent a unique class of ownership. They are equity instruments, but they behave remarkably like debt, occupying a mezzanine layer in the capital structure. Their “preference” is twofold: preference in dividend payment and preference in asset distribution during liquidation.

Key Characteristics and 2026 Nuances:

- Status: Owner (Limited). The holder is a shareholder but typically has no voting rights, except on matters directly affecting their class rights (e.g., varying terms, winding up).

- Servicing (The Dividend): Dividends are often fixed (expressed as a percentage of par value or a spread over a benchmark). CRITICAL DISTINCTION: Unlike debenture interest, preference dividends are not a legal obligation until declared by the board. They are typically paid out of distributable profits. If profits are insufficient, they may not be paid.

- Cumulative vs. Non-Cumulative: This is the critical 2026 feature. Nearly all institutional-grade preference issuances are now Cumulative. If a dividend is missed, it must be accumulated and paid in full before any common dividend can be distributed. Non-cumulative shares are almost exclusively regulatory capital (AT1) for banks.

- Redemption and Tenor: While technically permanent capital, many corporate preference shares issued in 2026 have defined Redemption Terms (e.g., at the option of the company after 7 years, or mandatory redemption after 10). They are almost never truly perpetual.

- Participating: A niche 2026 segment where preference holders, in addition to their fixed dividend, participate in surplus profits once common shareholders receive a defined threshold.

IV. Comparative Analysis: Debt vs. Mezzanine (The 2026 View)

The following chart is vital for internal strategic modeling. It visually overlays the performance characteristics of typical 2026 issuances, highlighting the cost and stability differences.

Direct Comparison: A Corporate Law Perspective

| Feature | Debenture (Debt) | Preference Share (Mezzanine Equity) |

| Legal Status | Creditor (Lien/Claimant) | Equity Holder (Owner) |

| Returns | Interest (Mandatory Coupon) | Dividend (Discretionary/Cumulative) |

| Cost of Capital | Generally Lower (Tax Deductible) | Higher (Paid post-tax, needs higher gross yield) |

| Tax Implications | Interest is a Tax-Deductible Expense (Issuer) | Dividend is paid after Corporate Tax. (Issuer) |

| Ranking | Senior/Unsubordinated (High Priority) | Subordinated to all debt, Senior to Common. |

| Maturity | Fixed Redemption Date | Technically Perpetual, but often with Redemption options. |

| Security | May be secured by charge (Secured) or unsecured (Unsecured) | Unsecured. Equity. |

| Voting Rights | Generally None. | Limited (only on class rights variation). |

| Impact on D/E Ratio | Increases Debt/Leverage | Increases Equity/Reduces Leverage |

| Default Consequence | Failure to pay = Default/Insolvency | Failure to pay = Non-payment (if non-cumulative) or Accumulation (if cumulative). No immediate insolvency. |

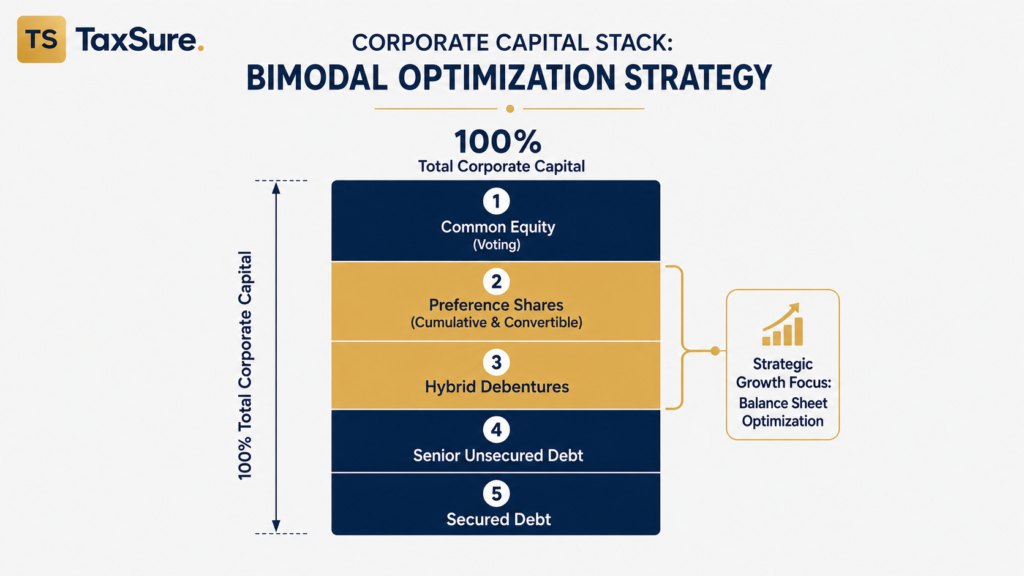

V. Strategic Application: Optimizing Corporate Capital Structures

A corporate strategy must utilize both instruments depending on specific scenarios. A robust 2026 capital structure is often a bimodal distribution, utilizing ultra-cheap secured debt where possible and strategic preference capital to manage covenant compliance.

Choosing the Right Instrument: The Taxsure Decision Tree

For boards contemplating issuance in 2026, we apply the following strategic framework:

1. Prioritize Debentures When:

- The primary goal is the lowest absolute cost of funds. Debt remains the cheapest capital due to the interest tax shield.

- Maximum tax deductibility is required to offset strong earnings (subject to local thin capitalization and Pillar Two rules).

- The company has stable, predictable cash flows that can comfortably service fixed debt obligations.

- The issuer is comfortable with strict restrictive covenants (e.g., leverage ratios, asset coverage, negative pledge) in exchange for lower yield.

- No dilution (even eventual) can be tolerated.

2. Prioritize Preference Shares When:

- Managing Debt-to-Equity and Leverage Ratios (EBITDA multiple) is paramount. Issuing preference equity strengthens the balance sheet (reducing “Net Debt”). This is critical for maintaining an Investment Grade Rating (BBB- or higher), which is highly valued in 2026.

- The company needs “Equity Credit” from rating agencies (which often treat cumulative preference shares as 50% or 100% equity).

- Servicing flexibility is needed. If cash flow is volatile (e.g., in growth phases or cyclical industries), the ability to defer dividends, even cumulative ones, provides a crucial buffer compared to mandatory interest.

- Traditional lending covenants cannot be met. Preference shares have few, if any, restrictive operational covenants.

- The company seeks capital that is permanent or at least long-tenor with deferred redemption.

VI. Accounting, Taxation, and Compliance in 2026

The legal and accounting distinction between these instruments is nuanced and jurisdictional. In 2026, compliance requirements are stringent.

1. The Accounting Divide (IFRS 9 and US GAAP)

For financial reporting, substance prevails over form. Under both IFRS and GAAP, the classification of preference shares is complex.

- Debentures: Are always classified as Financial Liabilities.

- Preference Shares: May be Equity, Liability, or a Compound Instrument. Shares that must be redeemed at the option of the holder on a fixed date, or have mandatory dividend triggers, are often classified as Liability, nullifying the balance-sheet advantage of equity classification. A carefully structured, non-mandatory-redemption preference share is essential for Equity classification.

2. Taxation (Pillar Two and Interest Deductibility)

In 2026, the OECD BEPS 2.0 (Pillar Two) global minimum tax rules (15% efficient rate) are fully operational for larger multinationals.

- Interest: Interest remains generally tax-deductible. However, Interest Limitation Rules (e.g., OECD Action 4) often restrict deductions to a percentage of EBITDA (e.g., 30%). For highly leveraged entities, debentures might generate “stranded deductions” that cannot be used.

- Dividends: Preference dividends are discretionary, paid from after-tax profit, meaning they offer no tax benefit to the issuer.

CFOs must model the effective after-tax cost (the ‘Weighted Average Cost of Capital’, or WACC) for each option, factoring in deduction limits.

3. Regulatory Compliance and Disclosure

Both instruments are Securities. Issuance in 2026 requires meticulous compliance:

- Prospectus and Registration: Issuances (especially to public investors) require detailed, approved disclosure documents (Prospectus) under jurisdiction-specific regulations (e.g., SEC in the US, ESMA guidelines in the EU, SEBI in India).

- Listing: Both are frequently listed on major stock exchanges to provide liquidity, triggering ongoing listing agreement disclosures.

- Sustainability (ESG): In 2026, Green Debentures and Sustainability-Linked Preference Shares are dominant. Compliance requires independent verification (Second Party Opinions) that the issuance proceeds align with environmental or social goals, subject to strict anti-greenwashing enforcement.

VII. Conclusion: The 2026 Taxsure Perspective

The capital market environment of 2026 does not favor simple solutions. The era of ultra-cheap, vanilla debt has passed. The most resilient and efficient companies will be those that strategically utilize the full spectrum of available instruments.

Debentures remain the efficient workhorse for non-dilutive, tax-advantaged financing when cash flows are robust and covenants are acceptable. Preference shares, however, provide the essential strategic buffer—strengthening the balance sheet, managing rating agency metrics, and providing servicing flexibility during periods of volatility.

Optimization in 2026 requires analyzing not just the instrument itself, but its interplay with accounting standards, global tax protocols, and rating agency methodologies. Our analysis concludes that a sophisticated 2026 capital structure is rarely either/or, but rather a dynamic mix, where hybrid structures and preference capital play an expanding and pivotal role in balancing risk, cost, and stability.

Disclaimer: The information provided in this article, including but not limited to text, graphics, images, and other material contained on this website, is for general informational and educational purposes only.

Leave a Reply

We value your thoughts and would love to hear your perspective.